Most predictions reflect the past. Stock market returns average about 9% a year.

Failure of Investment Fads

It’s once again time for the annual tradition when Wall Street observers stare into their crystal balls and tell us what we should expect for the next year. The funny thing is that no matter the situation, each year their predictions are remarkably similar. Over the last one-hundred years, the market has gone up about 7% a year. Add in dividends, and the stock market goes up about 9% a year. So, almost every year the top investment strategists in the nation forecast that history will repeat itself, and the market will go up between five and ten percent during the next calendar year.

These meaningless predictions are correct on average, but that doesn’t give us any unique insight into how we should position our portfolios for the year ahead. In fact, the more analysts agree on the forecast, the less likely it is to come to fruition. As insights become widely held, they’re no longer unique. Eventually, what was once an insight becomes the consensus.

People are susceptible to fads, and there is a lot of pressure to conform to what’s trendy. I’m guessing that if you were in junior high or high school in the mid-80s you owned a Swatch watch and acid wash jeans. Inevitably, fads lose their appeal at the point that everybody is on board.

Investment strategies can behave a lot like fads. The longer that a strategy or asset class outperforms the more widely adopted it becomes. Over-confident investors believe that a strategy is permanently superior and even infallible while the ground is crumbling beneath their feet. When a fad peaks and then crashes, it’s a long way down. Remember Spencer and Heidi?

Beware of the most crowded trades. Crowding occurs when too many investors believe the same thing.

The best investors take advantage of the limitations of conventional wisdom. To outperform the herd, you must exploit the herd. This starts by avoiding the areas that are most popular and in which investors are most confident. U.S. stock outperformance is a very long-running trend. The dollar is as strong as it has been in fifteen years. America’s share of the global stock market is also at a fifteen-year high.

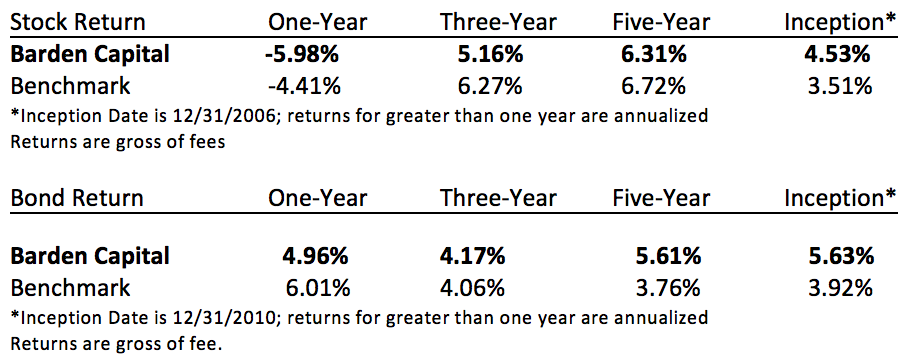

After such an extended run of outperformance, investor portfolios are likely over-weighted to U.S. stocks and underweight in international stocks. We maintain a roughly 35% allocation to international companies. Eventually, Europe will get its act together and the U.S. economy, which has led the world now for the last eight years, will take a breather. If the dollar weakens relative to international currencies, the performance of our international companies should lead the portfolio.

President Trump

Finally, our long national election is over. Mark McKinnon, a political operator from here in Austin said to those who voted for Hillary, “Maybe your greatest hopes aren’t going to be realized…probably your greatest fears aren’t going to be either.” Democrats have long pushed for many items on Trump’s agenda, including reform of veterans’ hospitals, paid maternity leave, and improving roads and airports. Big, permanent changes require the support of both parties. The Democratic minority will work with President Trump when they agree with him and vigorously fight him on areas where they oppose his agenda.

Early indications are that economic stimulus is the top priority for the Republicans.

The market is trying to process what all of this means for fiscal policy. The early impression is that tax cuts are probable, most likely for corporations. The goal will be to incentivize corporations that have stashed profits overseas to bring that capital back home and invest in U.S. based projects. A combination of tax reforms and investment incentives could potentially achieve this result.

Democrats are likely to support an increase in spending on airports, roads, and bridges. Trump is promising world class infrastructure. Estimates are that this will require about $3 trillion. He also promises to increase defense spending. The combination of infrastructure and defense spending will provide a huge jolt to the economy. Adding in his proposal to cut taxes by more than $4 trillion, we could get more than $7 trillion in fiscal stimulus.

No one knows the impact of this kind of stimulus on inflation. Jeffrey Gundlach, the highly respected bond fund manager, predicts that interest rates will increase from about 2% today to 6% by the end of Trump’s first term as a result of higher inflation.

Higher inflation is generally positive for stocks, but negative for bonds.

When inflation increases, stocks tend to benefit, as corporations can increase prices for the goods and services they provide. Bonds tend to suffer as inflation forces interest rates higher, which decreases the value of lower yielding bonds.

So far, the Trump victory is turning capital markets upside down. It seems likely that the playbook that has worked for investors over the last ten years is unlikely to work as well over the next five years. When Washington D.C. is under the control of one party, legislation tends to move more quickly. We’ve become used to a gridlocked government. Now, investors must factor in a more active government.

The Federal Reserve is raising interest rates, and now it appears that fiscal policy will become much more stimulating to the economy. This could signal the end of the era of bond outperformance and be the beginning of a period where stocks do better than usual.

No recession in 2017

Market Outlook

The probability of an economic downturn in the next year is very low. Contrary to most people’s expectations, economic expansions don’t die of old age. An external factor like the Federal Reserve raising interest rates too much, or a crisis in the banks typically occurs before the economy turns down. Strong growth in employment should support higher consumer spending next year. Interest rates are still very low which should support long-term capital investments.

We’re still in the slow and steady phase of the economic cycle, but Europe and Asia are likely in the early stages of their current economic expansions. Employment growth in Europe is even stronger than in the U.S. and interest rates are low.

I can’t speak to how stocks or bonds will perform in the next year. It is more productive to look at how the economy will perform next year and what will be the likely the fundamental impact on our companies.

In the case of the current expansion, we are living through one of the slowest economic recoveries on record. The biggest benefit of the lackluster pace of the expansion is that the economy is less likely to overheat and less likely to require excessive Federal Reserve intervention, which would increase the risk of a downturn. Corporate strategies are more productive as the slow and steady economic backdrop makes it less likely that companies will make major miscalculations in their capital investments.

Political turbulence doesn’t necessarily mean market turbulence

I’m optimistic that most of the turbulence over the next year will remain confined to the political arena and stocks will deliver average to above average returns. Our goal is to maintain exposure to a broad array of opportunities around the world. We have very high quality companies that are performing well and that are trading at reasonable valuations relative to their future expected returns.